After 2016, ushered in 2017, many people are writing industry trends.

I don't have the ability to write down some of my versatile views at the beginning of the year, and I am going to look at it by the end of this year.

This article talks about the hot Internet of Things.

Basic knowledge of the Internet of Things

The Internet of Things is a hot spot for all parties, including operators. What are the business opportunities around the Internet of Things?

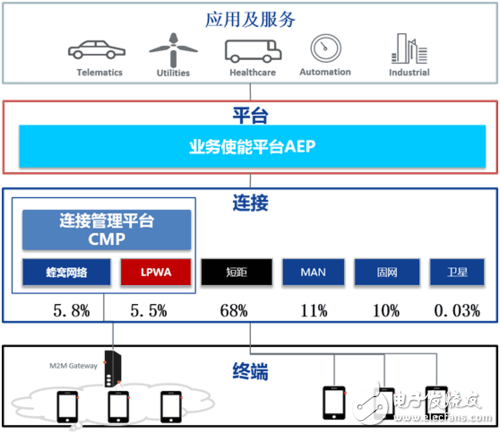

This is the overall block diagram of the Internet of Things.

We divide the Internet of Things into four levels, one by one.

The terminal layer represented by intelligent hardware is the final carrier used by the user, and bears the functions of information perception, data collection, command response, and execution.

Connections are the foundation of the Internet of Things. They can also be divided into two categories: one is a carrier connection represented by cellular and LPWA (Low-Power Wide Area Network), and the other is a non-traditional wireless connection represented by Bluetooth and Wifi. Or wired connection. CMP (Connection Management Platform) is a tool and platform for operators to manage connections. Popularly speaking, it is the BOSS+ network management support system of the Internet of Things.

The application of the Internet of Things is very diverse, and it is characterized by its strong professionalism and lack of economies of scale. Therefore, it is very important to achieve a platform for cost reduction and efficiency enhancement for applications, and AEP (Application Enablement Platform) is the representative. Through the cloud open interface and other means, the developers and applications of the Internet of Things provide development tools, operating environment, terminal management, data aggregation processing, business analysis, intelligent decision-making and other auxiliary capabilities to promote the value of the Internet of Things.

The top-level applications and services are the key to the IoT value redemption and business operations, and the most active areas. Nowadays, this field is intertwined with hot topics such as big data, artificial intelligence, and virtual reality. The data and information acquired by the terminal are processed and processed, and the interaction between various people and things or objects is realized.

Next time someone will say to you that you are engaged in the Internet of Things, you can ask: What layer of products are you doing?

The operator's focus is on connectivity or platform

Compared with many enterprises around the Internet of Things industry chain, operators with high financial resources and high self-esteem have tried to invest resources in terminals, connections, platforms, applications and other aspects.

In the terminal field, all three operators have relatively independent terminal companies and have extensive experience in leading the industry chain. On the other hand, all three operators are looking for investment targets in the fields of modules and chips, trying to profit from the Internet of Things feast through capital operation.

In the field of application, operators also have independent teams working on development, hoping to take advantage of the resource advantages of operators, early contact with customers and understanding of needs to form a first-mover advantage; but as time goes by, more and more people It is realized that the disadvantages of the operators' mechanisms, costs and knowledge structure are ultimately manifested in the market, and the lack of competitiveness, especially the low efficiency and slow response, may not necessarily stand out.

Gradually, operators are focusing on the two aspects of connectivity and application. Among them, the connection is the domain that the operator is best at, and the platform is the key to the operator's future breakthrough.

What operators are best at is building networks to put users, from telegrams to phones, from fixed networks to mobiles, from 2G to 4G. The network construction department is not afraid of hardships and hardships, and the hard-working environment can also build the network; the market business department is not afraid of early greed, and the higher indicators can be completed. The operating businessman used to be very proud: there is such a fighting power, what else can't be done?

However, when it comes to 5G, the choice of LPWA technology is not so easy: NB-IoT and eMTC have their own advantages and disadvantages, which makes it difficult for operators who have the characteristics of Libra.

Moreover, even if the network is built, what are the benefits of cellular and LPWA networks?

In terms of quantity, the number of connections carried by the carrier network accounts for only about 10% of the total number of IoT connections;

From the perspective of revenue, the income of the ICT card is one tenth or even one-thirtieth of that of an individual customer.

This means that if operators continue to use the current operational and management model to develop IoT connectivity, it is using low cost to achieve low returns, and the prospects are worrisome.

Looking at the platform level, there is an opportunity. In the initial stage of the Internet of Things, many applications need to reduce development costs and respond quickly to market goals. A good platform is popular among application developers. At this time, who can provide a cloud-based development platform, low-cost infrastructure, and open access management, so many players can contribute massive amounts of data and diverse applications. The ecosystem of the Internet of Things is not formed on this platform. Possible things.

More importantly: the operator's actions in this regard are not too late, and the starting point is not low. Take China Mobile's Internet of Things company OneNET as an example. At present, hundreds of enterprises have access, and the connection point has already exceeded one million mark. It should be known that these connection points are not just through the operator's network. In practice, the Internet of Things company has found an AEP, which is very valuable.

So now the question is coming: Should the operator's next development focus be on connectivity? Or should it be on the platform side?

Making a large connection scale is what traditional operators are best at, but the value of the Internet of Things connection is not high. Operators will make the scale of the connection, network construction and marketing costs will not be low; but is this the basis for the Internet of Things? If operators try to make more money through their own connections, they may lead the industry chain to develop non-operator connections, and by then there may be a basket of water.

If the focus of work is on the platform side, the biggest risk for operators is how to grasp the scale of “for†and “not forâ€. The platform must not only reflect its own value, but also play the enthusiasm of its partners. In this respect, it must have a strong control ability at the technical level. More importantly, it should establish the idea of ​​service and understand the true meaning of "Enable". We have seen a lot of operators have built a platform, and then the partners will use the platform as the power to rent-seeking. There is such a mentality that it is not a good platform.

Is the operation of the Internet of Things centralized or maintaining the status quo?

Previously, China Mobile has done more than a year of research projects, trying to find the best development path for the Internet of Things.

When making strategic planning from the top down, this conclusion seems to be self-evident: the Internet of Things has a low unit price and a high degree of business standardization, which is most suitable for centralized and unified operation of the entire network.

Through research, we can see that the traditional two-level operation model is no longer suitable for new business development such as the Internet of Things. The Internet of Things company launched a product innovation. Before going online, it must confirm the demand with the business department. Then the headquarters support department issued a two-level transformation plan. The headquarters and the provincial company were separately transformed, and then the network was commissioned. When the line was finally launched, the distance demand was raised. It has been 3 months. If the demand changes during this period, the entire transformation work will be terminated, and the demand adjustment will start from the beginning.

In contrast, China Unicom and JASPER platform cooperation, the business network unified standards, the platform side has given a complete solution and requirements template, the account manager only needs to configure the product according to the authority, you can go online immediately.

It can be seen that in the era of the Internet of Things, the ability to billing, product management, resource allocation, and other business support/network support needs to be concentrated in order to usher in the great development of the Internet of Things. Only a centralized model can minimize costs, compress business online time, and compete with Internet companies.

When the centralized thinking was basically formed, we also investigated the actual situation of the provincial company and found that the style of painting changed.

Although China Mobile has developed nearly 100 million IoT customers, about half of them use local networks. When asked why they don’t use the IoT private network, it is difficult to meet the innovation needs of IoT companies. .

It can be imagined that with the nationwide concentration of support systems, the degree of business standardization will be greatly improved compared with the present. The individualized needs of different regions need to pass the layer-by-layer approval and demand scheduling, and the business online progress cannot be compared with local development. Therefore, the national centralized support platform will face tremendous pressure on the individualized needs of the entire network.

Obviously, the high cost of localization support is difficult to support the great development of the Internet of Things, and it lacks the ability to respond quickly to the unified requirements and rules of the entire network. However, localized innovation is still an important driving force for the development of China Mobile. The construction, operation, management and marketing of communication networks and connections are still the main force of the company. How to resolve this contradiction?

If we insist on the centralized road, the cost of connection expansion will fall; but the individualized demand of the local companies is slow, and we can only rely on the unified products of the whole network to expand the Internet of Things. If all innovations and actions must be based on a unified platform across the entire network, how much space does the provincial company have to expand its business? Still willing/willing to pick up the KPI for the development of the Internet of Things? Will it repeat the mistakes of China Unicom's 3G era, and miss the opportunity for user development in order to push the centralization?

If you don't concentrate, then I have to sigh with it: If the Internet of Things cannot achieve centralized national unity, how many businesses and products are suitable for the whole network?

Conclusion

JASPER is the world's largest CMP supplier with more than 3,500 customers and 25 IoT service providers, using its platform across 100 countries for a long time. At the beginning of 2016, it was acquired by Cisco for $1.4 billion.

Many people may be surprised, why do I use the word "zone". Because JASPER is the leader in the Internet of Things CMP field, it has a large number of customer data, user connection information, mature IoT operation mode, and a global support system. The financial situation is also good, why only sell for 1.4 billion US dollars. Is the value much lower than many IoT start-ups?

There is only one answer: in the future, the connection is not worth the money.

What are we still hesitating? Where is the solution? After reading my article, do you understand?

Low volatge panel distribution system with CCC Certificate:

. Customized low volatge panel

. LV distribution

. MCC system

. Lighting system

. Air conditioner control system

. Fire protection system

Lv Panel,Lv Distribution,Low Voltage Panel,Low Voltage Distribution

Guangdong Superwatt Power Equipment Co., Ltd , https://www.swtgenset.com